3 min read

The Layman's Guide to Gasoil Hedging with Futures

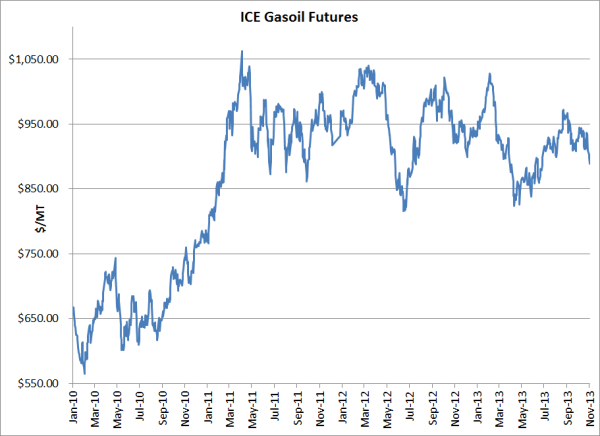

As many companies are beginning to plan for 2014, we have received quite a few inquiries from companies who are looking into hedging their gasoil...

2 min read

3 min read

As many companies are beginning to plan for 2014, we have received quite a few inquiries from companies who are looking into hedging their gasoil...

2 min read

As we discussed yesterday in The Layman's Guide to Natural Gas Options - Part II, there are four primary variables that affect the premium or price...

1 min read

As we discussed in our last post, The Layman's Guide to Natural Gas Options - Part III, there are four primary variables that affect the premium or...