Before we head out for the long weekend we thought we should address the current state of the natural gas market as it relates to hedging, for both producers and consumers, as we received several calls today asking for our two cents.

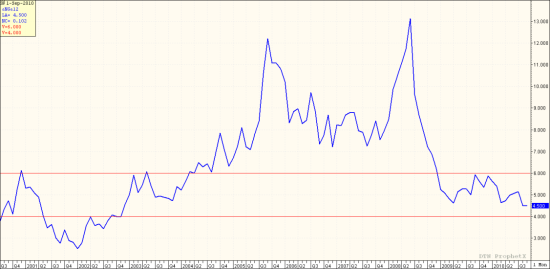

As many of you are aware, the one year forward strip (which is the average price of the first 12 months of NYMEX natural gas futures contracts) is currently trading around $4.50/MMBtu, near an eight year low. To find the last time the one year strip traded near or below the current level, you'll need to get in your time machine and travel back to 2002.

So, what's an unhedged or underhedged natural gas producer or consumer to do with prices at the current level?

If you're a natural gas consumer that is currently unhedged or underhedged, we would suggest that you strongly consider hedging at least a portion of your expected demand in the not too distant future. Sure, natural gas prices could very well continue to decline, but most commercial and industrial consumers would do very well with $4.50 gas over the coming year. As always, you need to determine your company's hedging goals and objectives as well as your budgetary needs before entering into any hedging transactions.

If you're a natural gas producer, you're obviously not thrilled with the current state of the forward curve. While the 12 month strip is near $4.50, the 24 and 36 month strips aren't significantly more attractive at $4.80 and $5.05, respectively. Which begs the question, will prices improve in the near future? Unless we experience an unanticipated event (a hurricane hitting the Gulf Coast, an extremely cold winter, etc.) it's difficult to have an educated, bullish opinion.

If one takes a quick glance at the fundamentals, all signs point towards flat or declining natural gas prices for the foreseeable future.

- Economy: No matter how you look at it, the economy isn't going to produce a quick or strong turnaround which means that unless it's weather related, natural gas consumption shouldn't increase significantly anytime soon.

- Storage: While inventories are slightly lower than this time last year, they're still at a very comfortable level vs. the five year average.

- Production: While the report out of the EIA on Monday showed that June output fell for the first time since December, estimates show that production is on track to finish the year at the highest level in nearly 30 years, approximately 22 TCF.

- Consumption: While total U.S. natural gas consumption has increased by about 1.8% over the past 10 years ('99-'09), including a 43% increase from power generation, industrial/manufacturing demand has declined by approximately 25% over the same period. The net of the these, over the past 10 years, only amounts to an approximately 1% increase as the industrial demand lost far exceeds the increase from electrical generation.

- Rig Count: The Baker Hughes report out this afternoon puts the current, natural gas rig count at 977, four more than last week. As a result, the current rig count is nearly 50% higher than last July when it bottomed at 665.

Perhaps all of the above will prompt producers to slow drilling which should, in turn, push gas prices higher but given that the rest of the fundamentals are what they are, we wouldn't bet on it.

Enjoy the long weekend.